🚨 The Mechanics of Gamma (GEX) : How Dealer Hedging Actually Moves Markets

Gamma is one of the most powerful yet misunderstood forces in options trading. While most traders focus on direction or volatility, gamma represents the rate of change of delta -and it is the primary reason why markets can pin, squeeze, or break violently even when fundamentals remain unchanged.

This article elucidates the fundamental mechanics of Gamma using clear visuals and precise concepts that even novice traders can understand. It is specifically tailored for the Indian options trading community, addressing the lack of clarity regarding the concept and its application. We are intentionally avoiding the mathematics of Gamma exposure in this blog to keep it simple. Additionally, we have observed on X that some self-proclaimed ‘guru’ experts use such jargon to market their courses, leading to misunderstandings among traders.

Gamma Regimes: Why Markets Pin or Accelerate

Gamma is not a single force- it operates in two opposing regimes depending on whether dealers are net long or net short gamma. Understanding this distinction is essential for interpreting why prices sometimes stick stubbornly to certain levels and at other times explode away from them.

1. The Two Gamma Regimes

Market makers/dealers who are short options are typically short gamma. However, the net gamma position across the dealer community determines market behavior.

- (A) Long Gamma Regime (Positive Net GEX): Dealers are net long options. To stay delta-neutral, they sell as price rises and buy as price falls. This is counter-trend hedging. It dampens volatility and creates a magnetic effect around high open-interest strikes.

(B) Short Gamma Regime (Negative Net GEX): Dealers are net short options. They are forced to buy as price rises and sell as price falls. This is trend-following hedging. It amplifies moves and can produce violent squeezes or breakdowns.

The same mechanical hedging process produces opposite outcomes depending on the sign of net gamma.

Without going into mathematics , simply directionalize GEX can be written in form of :

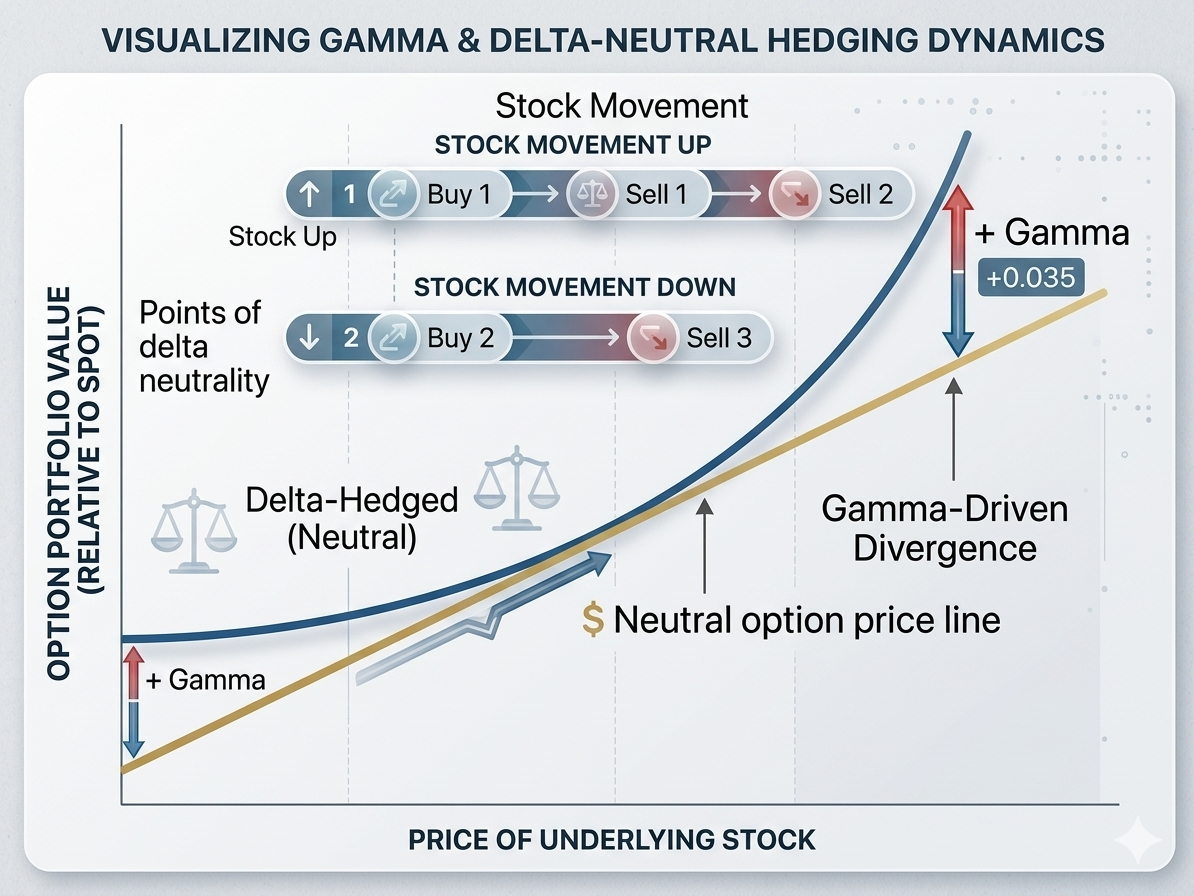

(A) Long Gamma: The Source of Pinning and Mean-Reversion

When dealers are net long gamma, their re-hedging activity pulls price back toward high-convexity strikes. This is the true mechanical driver of pinning.

The diagram below illustrates long gamma scalping behavior. As the underlying moves up, the long gamma position requires selling into strength (Sell 1, Sell 2) to remain delta-neutral. As price falls, the position requires buying into weakness (Buy 1, Buy 2). This “buy low, sell high” dynamic creates a stabilizing force around strikes with concentrated gamma. This constant re-hedging is not discretionary-it is a mathematical necessity driven by convexity.

Key Equation ( to avoid complex mathematics) :

When gamma is positive and large, even modest price changes (ΔS ) trigger meaningful counter-trend hedging flows. This is why price often exhibits magnetic behavior near strikes with heavy open interest when the dealer community is net long gamma.

(B) Short Gamma: Acceleration and Squeeze Dynamics

When dealers are net short gamma, hedging flows reinforce the direction of the move rather than opposing it as illustrated in below figure which is self explanatory.

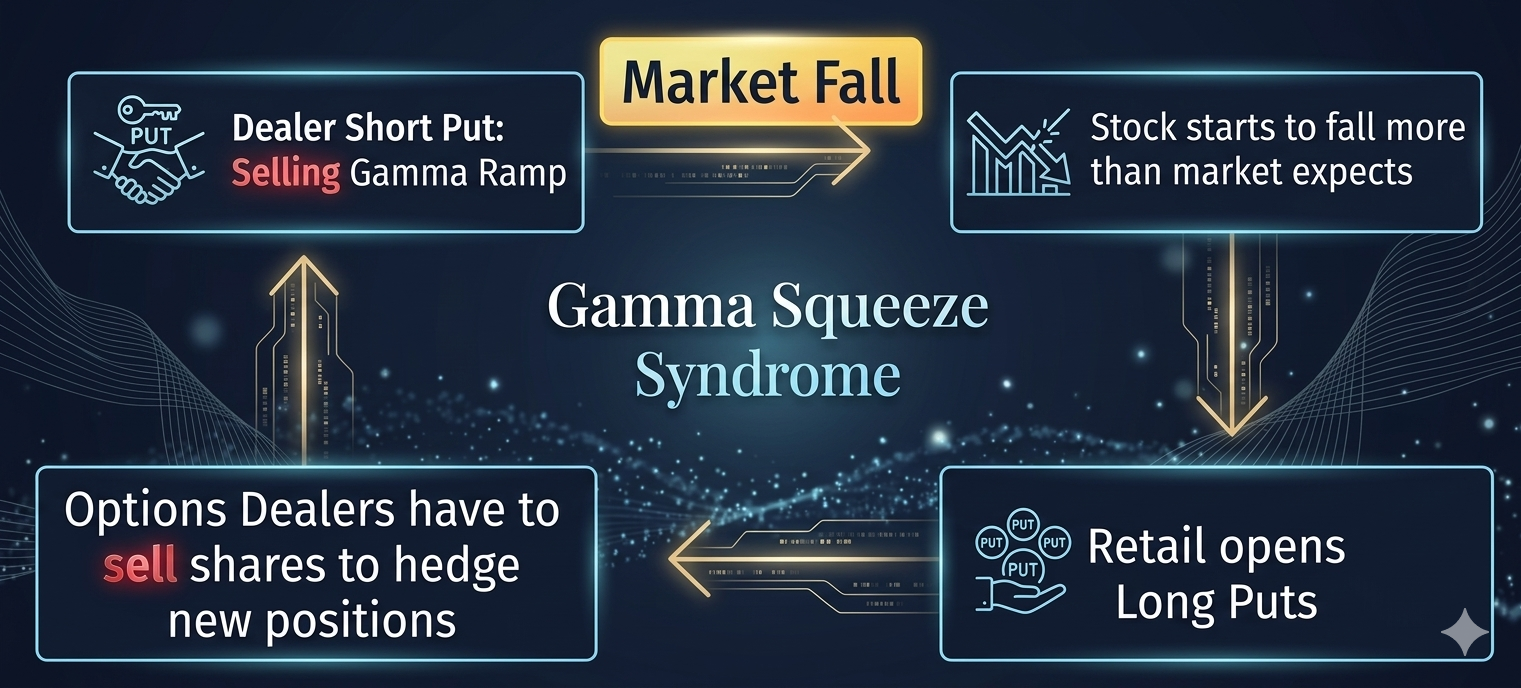

Short Put Position (Deflating Gamma Ramp):

As price falls, delta becomes more negative. Dealers must sell shares to re-hedge. This adds selling pressure, causing price to decline further than it otherwise would. As shown below the feedback loop in case of short dealer put gamma when market falls.

Short Call Position (Squeezing Gamma Ramp):

As price rises, delta becomes more positive. Dealers must buy shares to re-hedge. This adds buying pressure, causing price to rise further than fundamentals alone justify. This ipsilateral (same-direction) hedging is the core mechanism behind gamma-driven acceleration.

The two diagrams above show Gamma Squeeze Syndrome in both directions. Whether the market is falling (short puts forcing share sales) or rising (short calls forcing share purchases), the mechanical response of short gamma dealers amplifies the move until either gamma decays, dealers reduce risk, or a regime flip occurs.

When retail and institutional flows align against short gamma dealers, the hedging response can create self-reinforcing moves known as Gamma Squeeze Syndrome. In both cases, dealers are hedging in the same direction as the price move (ipsilateral hedging). This turns normal trends into accelerated moves and explains why liquidity can appear deep before suddenly evaporating.

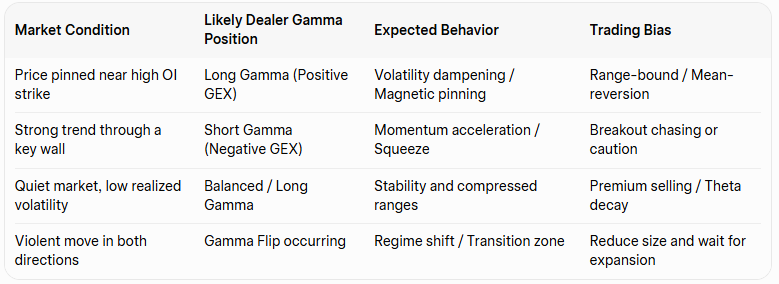

Practical Framework: Reading Gamma Regimes

The following table aligns market conditions with the correct gamma regime and expected behavior:

“Is the gamma ladder still stabilizing, or has it flipped into squeeze mode ?

Final Note

Gamma hedging is the hidden engine room of options markets. Dealers do not "defend" levels out of conviction - they re-hedge because their risk systems demand it. Understanding whether that hedging is deflating or squeezing, and whether it is being overwhelmed, gives traders a structural edge that goes far beyond traditional technical analysis.

The most robust approaches treat gamma not as a static wall on a screen, but as a dynamic regime indicator that reveals when markets are likely to pin, trend, or squeeze. The same strike can act as a magnet or a launchpad depending on whether the dealer community is net long or net short gamma. The hedging flows themselves are mechanical; only the sign of net gamma determines whether those flows stabilize or destabilize price.

Master this distinction, and many seemingly random price moves begin to make structural sense.

Traders who can distinguish between these two regimes - rather than treating all gamma walls as equivalent: gain a structural lens into market behavior that goes beyond conventional price action or order flow analysis.

Disclaimer: The content of this post is purely educational and derived from standard textbooks. It does not constitute investment or trading advice, including the buying or selling of indices, in any financial market.

0 comments

No comments yet. Start the discussion.

Leave a comment

Your email is required but never shown publicly.