Volatility Trading: Definition, Motivation, and Trading Objects

A substantial part of professional option trading focuses strictly on volatility while deliberately ignoring the direction of the underlying market. Volatility traders speculate on whether realized volatility will exceed or fall short of implied volatility, and whether implied volatility itself will rise or fall. In short, they care more about how much the underlying price changes than about the direction in which it moves.

Why Trade Volatility ?

Just as equity/index investors/traders believe they have an edge in forecasting the direction of stock/indices prices, volatility traders believe they can foresee the level of future (implied) volatility. If current volatility appears low, a trader may want to take a position that profits if volatility increases.

One of the key attractions of volatility trading is that forecasting directional moves in the underlying asset is notoriously difficult, whereas volatility can often be predicted with significantly higher accuracy. This makes volatility a more attractive "asset class" for many sophisticated traders and hedge funds.

What Exactly Is a Volatility Trade ?

Before discussing specific strategies, it is important to define what constitutes a volatility trade.

Definition: A volatility trade (or volatility trading strategy) is a position or portfolio whose value is affected only by changes in volatility (either actual/realised or implied, or both), while having no or only minimal exposure to the direction of the underlying asset.

Because volatility trades are designed to be delta-neutral, they are also referred to as market-neutral or non-directional trades with respect to the underlying asset.

It is useful to distinguish between two types:

- Directional volatility trades: The trader has a specific view on the level or movement of volatility.

- Nondirectional (relative) volatility trades: Also referred to as volatility arbitrage, these strategies attempt to profit by exploiting volatility differences across different markets or instruments.

In this article, we will focus primarily on directional volatility trades.

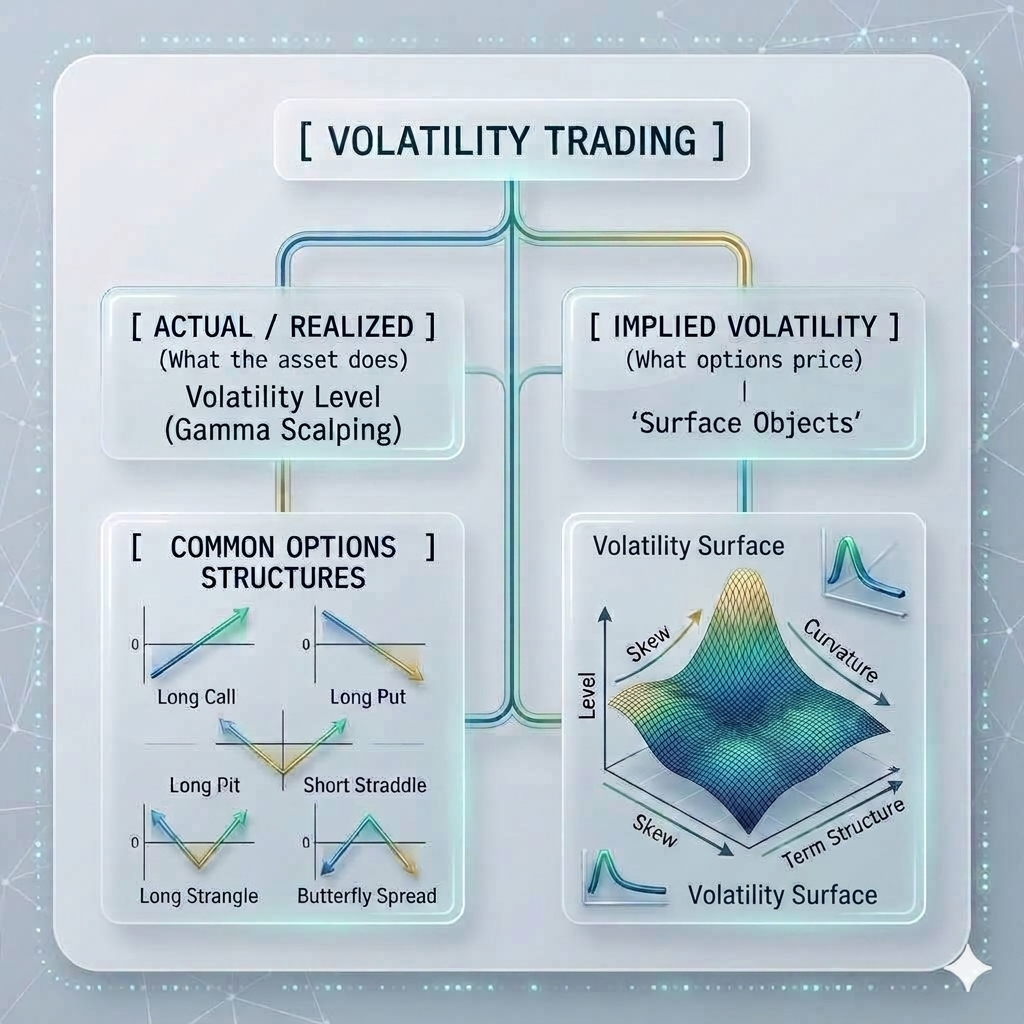

Volatility Trade Design: Trading Objects

When initiating a volatility trade, a trader/investor typically has a view on a specific aspect of volatility. Because there are multiple concepts of volatility, it is essential to clearly define the trading object - that is, the precise type of volatility being traded.

Broadly, volatility trading objects can be divided into two major categories:

1. Actual / Realized Volatility

This class of trades focuses on the level of actual stock/indices price volatility. Success depends on whether the trader can forecast future realized volatility better than the market. The key comparison is between ex-ante expected volatility and ex-post realized volatility.

Realized Volatility Mapping

Object: Volatility Level (Realized)

What It Means: The actual volatility experienced by the underlying asset over time.

Primary Strategy: Delta-Hedged Options (Gamma Scalping for long vol, or dynamic rehedging for short vol)

Key Insight: P&L is driven by the difference between realized volatility and the implied volatility at which the option was traded.

2. Implied Volatility (and the Volatility Surface)

The second class of trades focuses on changes in implied volatility or the implied volatility surface. This is where most sophisticated volatility trading takes place.

Once we move to implied volatility, things become more interesting because the market prices options across many strikes and expiries. This creates a volatility surface with multiple tradable dimensions.

Here’s how the major objects map to options structures :

| Volatility Object | What It Represents | Common Options Structures | Primary Risk/Exposure | Typical Market View |

|---|---|---|---|---|

| Volatility Level | Overall height of implied volatility | Straddle, Strangle, Delta-Hedged Options Portfolios | Vega & Gamma | "Vol is cheap/expensive" |

| Smile Slope (Skew) | How implied vol changes with strike | Risk Reversal, Skew vertical spreads | Skew / Asymmetry | "Downside protection is expensive" |

| Smile Curvature | Curvature of the smile (wings vs body) | Butterfly, Condor | Tail risk / Kurtosis | "Extreme wings are mispriced" |

| Term Structure Slope | How implied vol changes with time to expiry | Calendar Spread, Diagonal Spread | Time / Calendar Vega | "Short-term vol is too high relative to long-term" |

These objects are not entirely independent. In particular, there is often a strong relationship between actual (realized) volatility and the level of implied volatility for a given maturity.

Volatility Trading: Objects & Options Structures summarizes in the chart :

We skip pure volatility products such as variance swaps, volatility swaps etc.. These will be covered in other blog posts.

Key Takeaways

- Volatility trading is fundamentally about having a view on volatility itself, rather than the direction of the underlying asset.

- A true volatility trade should be delta-neutral (market-directional neutral), while isolating specific gamma or vega exposures.

- Traders/Investors must clearly define their trading object -whether it is realized volatility, implied volatility level, skew, curvature, or term structure.

- Different volatility objects require different options structures to express the desired view effectively.

Understanding these distinctions is essential for designing consistent volatility trading strategies and for properly measuring and managing risk.

Disclaimer: The content of this post is purely educational and derived from standard textbooks. It does not constitute investment or trading advice, including the buying or selling of indices, in any financial market.

0 comments

No comments yet. Start the discussion.

Leave a comment

Your email is required but never shown publicly.